Key Takeaways from the 2013-2023 CBO Budget and Economic Outlook

Share

Share

Growth is expected to be slow in 2013, with just a 1.4% real increase in gross domestic product

On February 5, the Congressional Budget Office (CBO) released an updated Budget and Economic Outlook, which includes projections for fiscal years 2013 through 2023. The new “current law” baseline reflects tax and spending policy changes that were included in the New Year’s Day fiscal cliff deal.

Previously, for example, the baseline assumed that the 2001, 2003, and 2009 tax cuts would expire and the alternative minimum tax (AMT) would not be adjusted for inflation, thereby ensnaring tens of millions of additional taxpayers. Now that the majority of the aforementioned tax cuts and AMT indexing have been made permanent, the updated baseline reflects this. Because Congress was routinely extending these measures, the fiscal position of the nation has not changed in a material way, and CBO’s current law “scorekeeping” now reflects, for the most part, current policy.

CBO’s projections include important insights into the economy and the federal budget. Here are a few that BPC believes are particularly important:

The Economy

Growth is expected to be slow in 2013, with just a 1.4-percent real increase in gross domestic product (GDP) and continued high unemployment hovering around 8 percent. This largely reflects two elements of fiscal drag: 1) the end of the payroll tax holiday and the corresponding effect on consumer spending and 2) the slowdown in government spending associated with sequestration, which is incorporated in CBO’s baseline.

Congress could change this situation by replacing sequestration with a different approach, such as longer-term reforms to entitlement programs and the tax code. After 2014, CBO expects the economy to begin a strong expansion, with average growth of 3.7 percent between 2014 and 2017. Unemployment, however, will be slow to return to more typical levels, staying above 7.5 percent through 2014 and finally declining to 5.5 percent by the end of 2017.

What’s Happening with the Deficit?

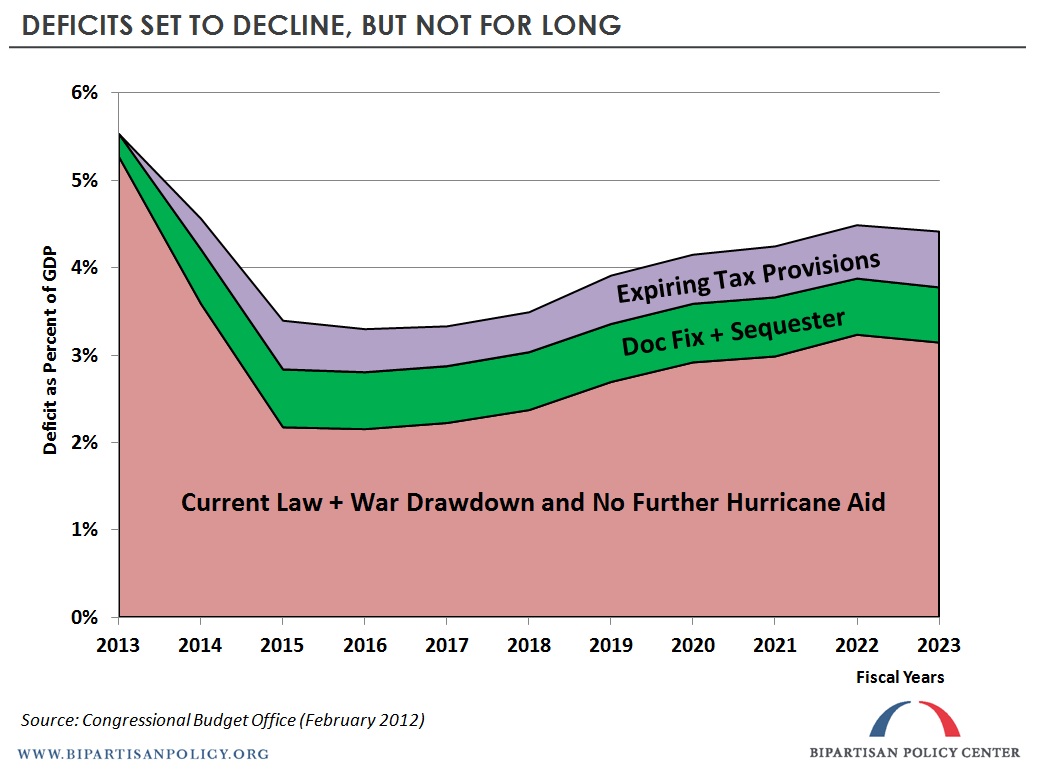

Under current law, deficits will decline over the next few years from over $1 trillion in Fiscal Year (FY) 2012 to $430 billion in FY 2015, resulting primarily from three factors: 1) Stronger economic and employment growth as the economy recovers; 2) Restrained defense and domestic discretionary spending from the caps in the Budget Control Act of 2011 and sequester; and 3) Increased revenues from taxes in the Patient Protection and Affordable Care Act (PPACA), the fiscal cliff deal, and expiration of the payroll tax holiday. After 2015, however, CBO expects deficits to once again increase rapidly, rising to $978 billion by 2023, at which point debt held by the public will reach 77 percent of GDP, nearly double the historical 40-year average, and be headed upward.

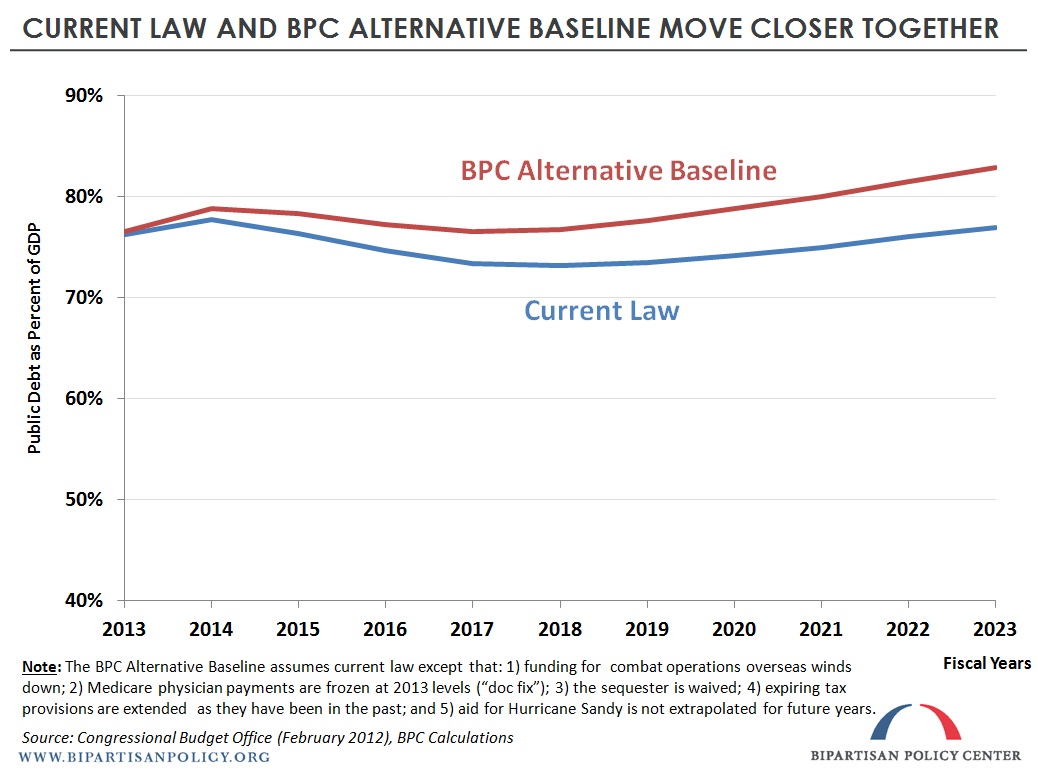

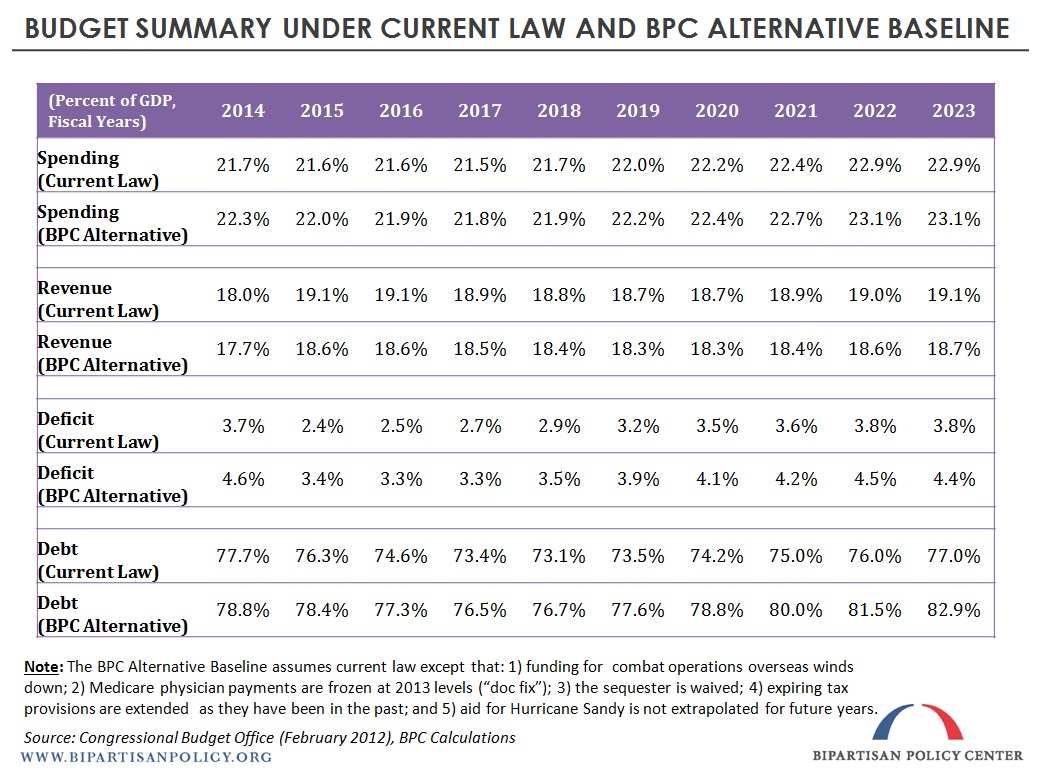

BPC has also modeled an Alternative Baseline, in which some policies that policymakers have routinely extended are reflected in the projections. Due to the fiscal cliff deal (as explained above), there is now a smaller difference between BPC’s Alternative Baseline and CBO’s current law baseline, but the distinction still helps to demonstrate the consequences of fiscal decisions. In particular, BPC’s Alternative Baseline assumes that 1) across-the-board sequestration cuts are cancelled; 2) expiring business and individual tax provisions are extended as they have been in the past; 3) physicians participating in Medicare continue to be protected from substantial cuts mandated by the Sustainable Growth Rate (SGR) payment formula; 4) overseas combat operations continue to wind down as scheduled; and 5) aid for Hurricane Sandy is not extrapolated for future years (i.e., we don’t have a devastating hurricane that requires emergency spending every year). Under these assumptions, debt held by the public in 2023 will stand at 83 percent of GDP.

Why Is the Debt Growing?

Ongoing deficits and increasing debt as a proportion of the economy are driven by the structural and soon widening mismatch between projected federal spending and revenues. CBO estimates that the additional taxes raised from the fiscal cliff deal will stabilize revenues at approximately 19 percent of GDP toward the end of the 10-year window, whereas spending will reach 23 percent of GDP by 2023 and then continue to increase.

Importantly, the 10-year window for which CBO issues estimates does not include significant projected increases in long-term spending related to health care costs growing faster than the broader economy. These increased costs are due in part to increases in Medicare eligibility due to the aging of the population, and the expansion of health insurance coverage to low- and middle-income individuals through Medicaid and insurance exchange tax credits and subsidies. Even if the debt were projected to be stabilized in the 10-year period, these upcoming costs would be worthy of great concern.

CBO provides several reasons for concern about the projected growth in debt is concerning. First, our current debt burden is already high by historical standards, well above the average levels that have prevailed since World War II.

Second, when the economy finally recovers from this prolonged slump, interest rates will rise from their historically low levels, significantly increasing the cost of servicing the debt. In particular, CBO projects net interest costs to nearly quadruple from $224 billion in FY 2013 to $857 billion in FY 2023. Higher spending on interest payments will compete with other public priorities, such as transportation, defense, medical research and education, and the large debt will crowd out capital that could be put to private investment, harming economic growth and job creation.

Finally, elevated debt levels limit the federal government’s flexibility should an emergency arise, such as another deep recession or a new overseas conflict. In a worst-case scenario, exploding debt could trigger a fiscal crisis, in which investors are no longer willing to lend money to the federal government at affordable rates.

Medicare Spending

Medicare spending is estimated to increase from 3 percent of GDP this year to 3.5 percent of GDP by 2023. That reflects a slowdown in Medicare spending that has occurred and CBO expects to continue for the next few years, at which point CBO expects that Medicare will once again grow faster than the economy as a whole.

The most substantial change from CBO’s March 2012 projections is for the Part D prescription drug benefit. For example, in that report, CBO expected Part D would cost $184 billion in 2022; in its updated projection, CBO expects that portion of Medicare to cost only $168 billion in 2022, a decrease of almost 9 percent. CBO’s new estimate for Part B (physician services) spending reflected a more modest decrease over last year’s estimate, and Part A (inpatient and post-acute) spending reflected a modest increase in CBO’s cost projections.

The change in projections for physician services’ costs has a very substantial practical implication: it dramatically lowers the “cost” of what is often referred to as a permanent “SGR fix.” Just last year, CBO scored a 10-year freeze in physician payment rates as increasing the deficit by $240 billion. Now, CBO projects the same 10-year fix would cost only $138 billion. (Note that a complete fix would probably be more expensive because physicians would likely be granted some annual update to account for increasing practice expenses.)

The New Baseline and the Next Three Cliffs (Take a look at our updated timeline)

With automatic sequestration cuts set to begin on March 1, followed by the expiration of the continuing resolution (CR) that is currently funding discretionary spending, and the April 15 deadline for each house of Congress to produce a FY 2014 budget resolution, Congress has three opportunities to address the near- and long-term budget and economic problems of the nation. In addition, policymakers will have to confront the debt ceiling again sometime this summer, a prospect that could again cause uncertainty for businesses and investors.

As CBO made clear, lackluster economic growth this year is directly related to the impending sequestration, and rising health care costs are directly related to the long-term upward growth trajectory of federal spending and debt. Congress could address both of these issues, along with reforming the nation’s tax code, to help the economy now and stabilize our debt over the coming years.

For more on BPC recommendations related to tax and entitlement reform, please see:

Related Posts

- H.R. 325, The Debt Limit, and Extraordinary Measures: A Technical Note (Warning: Wonky) January 31, 2013

- When Will the Next Debt Limit X Date Be? January 30, 2013

- Now It’s Time for Sequester Anxiety January 29, 2013

- The House Republican Debt Limit Proposal, Explained January 23, 2013

Share

Read Next

Support Research Like This

With your support, BPC can continue to fund important research like this by combining the best ideas from both parties to promote health, security, and opportunity for all Americans.

Give Now