Everything You Ever Wanted to Know About the Sequester

Share

Share

UPDATE: The Sequester: What You Need to Know, February 22, 2013

In the aftermath of the super committee’s demise, an updated look at the effects of the sequester

UPDATED MAY 18, 2012

By Loren Adler and Shai Akabas

Jonathan Goldstein contributed to this post.

Flashback to August of this year:

“But what happens if [the super committee] fail[s] to come to an agreement? That’s what the ?sequester’ is for. It will act as a ?sword of Damocles’ hanging over the JSC in the hopes of forcing action.”

Yes ? that was us writing. And, well ? hopes have since been dashed. But that means we get to do a fun second look at the effects of the sequester!

The Joint Select Committee on Deficit Reduction, which was established this summer under the Budget Control Act (BCA), was unable to agree on any savings. Nada. Zilch. That means that the rest of the savings from the BCA will be achieved by means of a sequester ? a triggered reduction of expenditures.*

Report

Indefensible: The Sequester’s Mechanics and Adverse Effects on National and Economic Security

A joint report from BPC’s Task Force on Defense Budget and Strategy, a joint effort of the Economic Policy Project and the Foreign Policy Project

June 2012

Section 302 of the BCA (which contains the legislative language on the implementation of the sequester), however, does not state clearly how the sequester will be carried out. Specifically, two possible interpretations of the sequester are: 1) It is intended to make cuts to discretionary appropriations and mandatory spending that add up to $1.2 trillion (less assumed debt service savings) over ten years (although no cuts occur in 2012, the first year), or 2) It is intended to reduce the deficit by $1.2 trillion (less assumed debt service savings) over the ten-year budget window. While at first blush these may seem identical, the former interpretation would produce significantly less deficit reduction in the first decade. This is primarily due to the timing difference between discretionary appropriations (the resources that are made available) and outlays (actual spending, which lags the appropriations).**

Related Posts

- The 2013 Sequester May Not Be What You Think

- Three Reasons Why $1.2 Trillion Isn’t Really $1.2 Trillion

The final decision lies with the Office of Management and Budget (OMB), but they have not yet made clear which interpretation they will use. For simplicity, the rest of this post utilizes the Congressional Budget Office’s (CBO) assumption that the sequester will be implemented as per the first interpretation ? that it is intended to make cuts to discretionary appropriations and mandatory spending that add up to $1.2 trillion (less assumed debt service savings) over ten years.

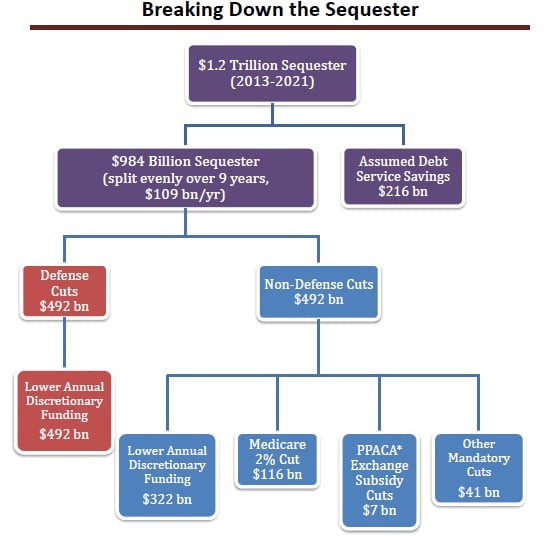

To view and share a larger version of the flow chart above, click here.

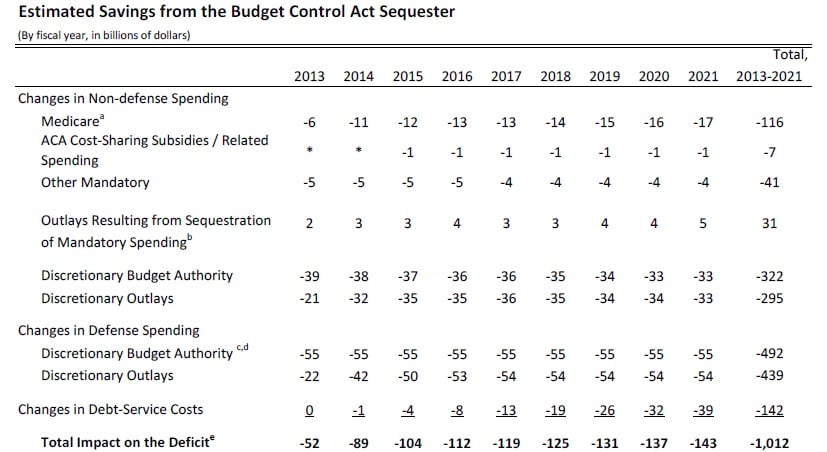

To view and share a larger version of the chart above, click here.

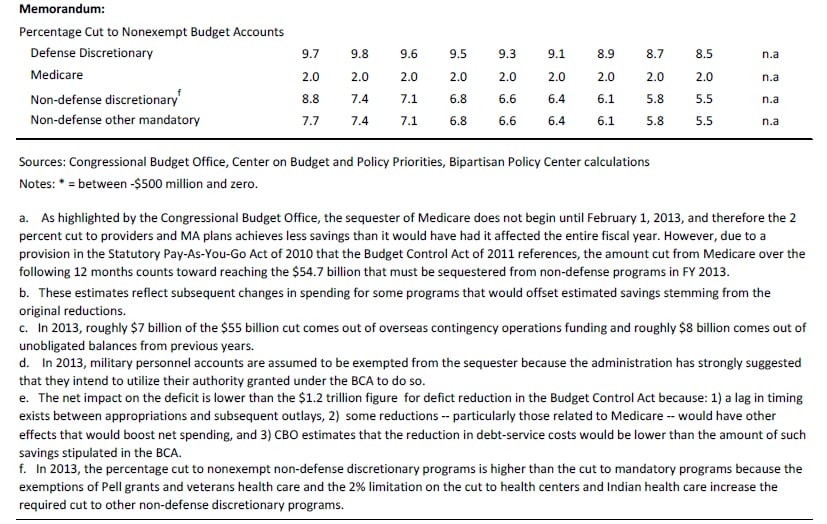

To view and share a larger version of the chart above, click here.

Beginning in 2013, OMB is required to cut $1.2 trillion from the budget for 2013-2021 in the manner shown in the above flow chart. For every year except 2013***, these cuts would be achieved by lowering the caps on defense (which does not include Overseas Contingency Operations) and non-defense discretionary budget authority specified in the BCA and by cancelling budgetary resources for some mandatory spending programs. OMB must abide by the BCA in carrying out the sequester, but there are a number of ambiguities and inconsistencies that the agency will have to interpret and resolve. The following, however, is clear:

- To account for the fact that part of the $1.2 trillion will come from debt service savings, the BCA instructs OMB to reduce the size of the sequester by 18 percent, to $984 billion.

- The dollar amount of the cuts must be evenly divided between each of the nine sequester years. Therefore, each year, OMB must sequester $109 billion from its baseline.

- The annual cut is split evenly between the non-exempt portions of defense (function 050) and non-defense spending, requiring approximately a $55 billion cut to each. Aside from exempt programs (of which there are many ? see below), these cuts are spread among both mandatory and discretionary spending.

- However, most mandatory spending is exempt from the sequester. Social Security, retirement programs, veteran’s benefits, refundable tax credits (such as the Earned Income Tax Credit and Child Tax Credit), Medicaid, the Children’s Health Insurance Program (CHIP), unemployment insurance, food stamps (SNAP), Temporary Assistance for Needy Families (TANF), and a host of other programs (mostly those benefitting individuals with low incomes) are all exempt from the sequester ? see the Statutory Pay-As-You-Go Act of 2010, starting on p. 22, for a list of all exempt programs. A cleaner list is also available here. Additionally, while most Medicare spending is subject to the sequester, the cut to Medicare cannot exceed 2 percent.****

For more detail on exactly how the cuts are calculated and distributed, see this previous blog post.

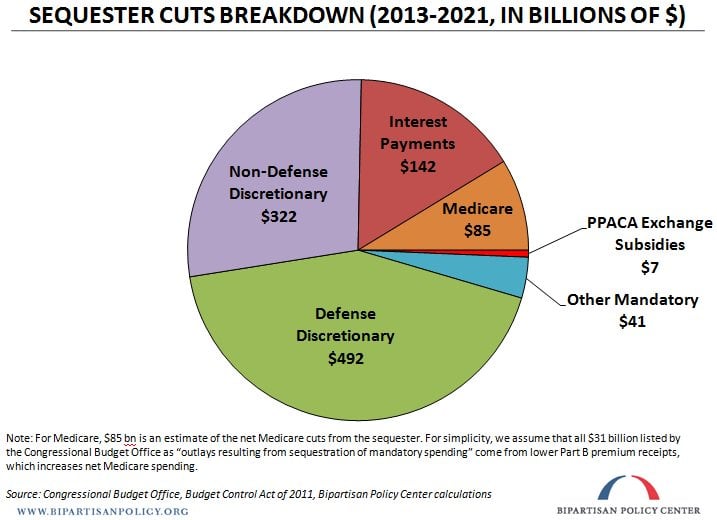

To view and share a larger version of the pie chart above, click here.

While it is possible at this point to specify the spending cuts to individual non-exempt mandatory programs, you may notice that we have not detailed what the sequester will mean for the discretionary accounts of each government agency. There is a simple reason for that omission.

As the flow chart above shows, the discretionary spending reductions that have been triggered by the super committee’s failure are (with the exception of 2013) applied to the total amounts that can be appropriated to defense and non-defense spending. Congress retains the power to decide how to distribute the pain across government functions within those totals. In other words ? assuming Congress is operating under regular order ? the initial imposition of the sequester squeezes (beyond the restraint imposed by the Budget Control Act) the topline defense and non-defense caps that the appropriations committees are charged to work with. As long as the sums of the 302(b)s (the appropriations subcommittee allocations) stay within those limits, however, any permutation of departmental allocations is allowed. For fiscal years 2014-2021, the “across-the-board cut” for defense or domestic discretionary spending is triggered only if Congress exceeds the new topline cap for that category in any given year.***

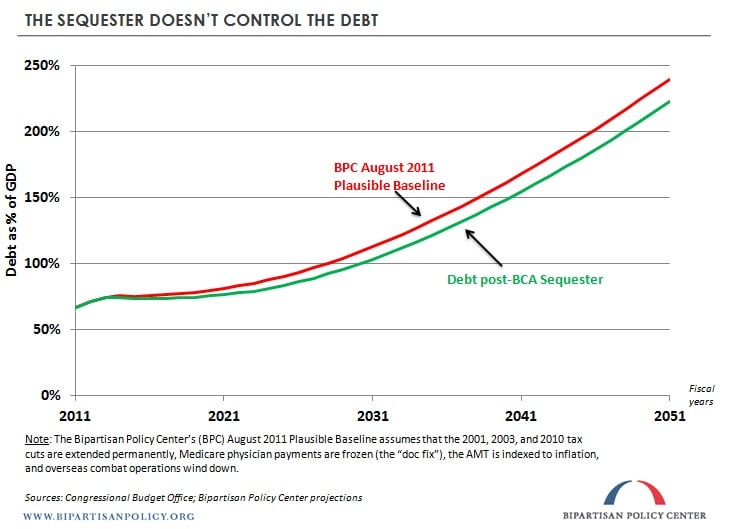

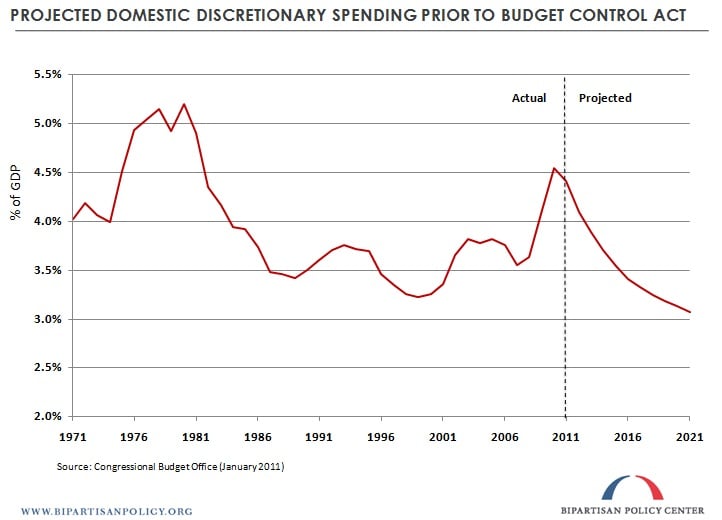

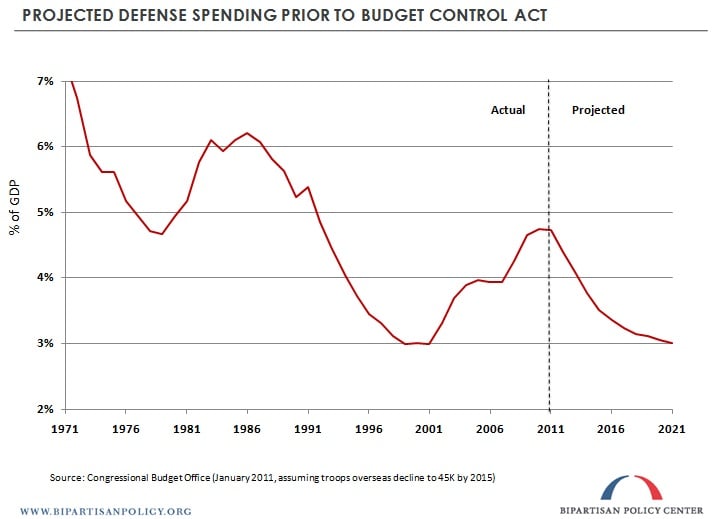

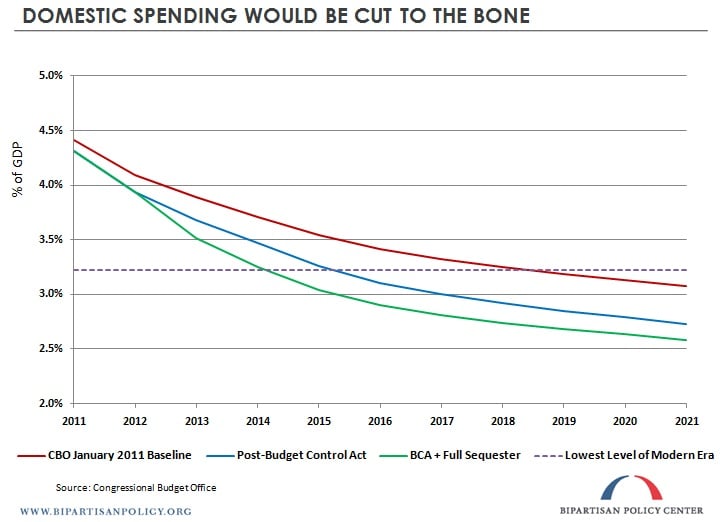

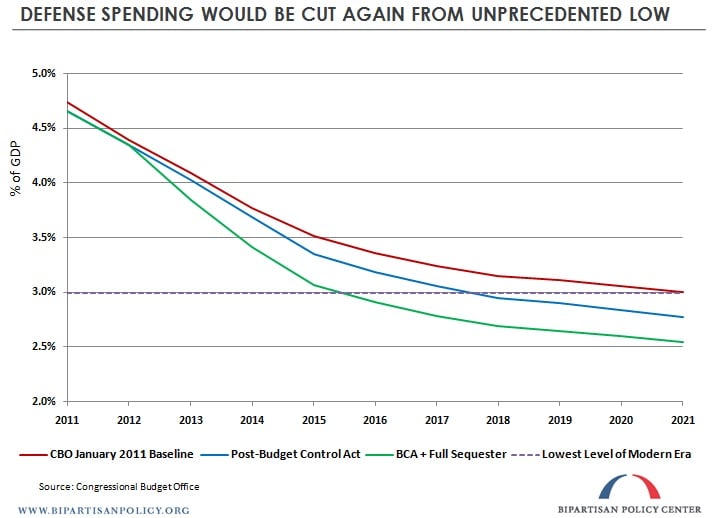

At this point, it is worth taking a step back to give a bit of context. These sizeable cuts to both defense and domestic discretionary spending will bring each of those levels down to historic lows as a percentage of the U.S. economy (see the end of this post for graphs). And for all that trouble, policymakers will have accomplished little in the scheme of stabilizing our debt. They may feel that they have pushed off the urgency of dealing with the problem for a few years, but the general trajectory remains unchanged.

To view and share a larger version of the graph above, click here.

Another consideration moving forward ? beyond the direct impact that the sequester’s cuts will have on defense forces and domestic programs ? is the uncertainty that departments will face if fiscal year 2013 has begun (in October 2012) and Congress has not yet definitively settled whether a sequester will take place. If the battles go into this year’s lame duck session, department heads will be forced to allocate funds without knowing their full budgets for the year. This is a recipe for disaster.

Steve Bell, former staff director of the Senate Budget Committee and now Senior Director of our Domenici-Rivlin Task Force, has described the sequester as “the longest telegraphed punch in history.” Congress should either brace for the blow with the leadership of both parties agreeing that the cuts will take place, or dodge the hit well in advance by offsetting the scheduled cuts with an equal or greater amount of alternative deficit reduction. The worst-case scenario would be a prolonged hesitation, whereby the issue remains unsettled ten months from now. That wavering could lead to the equivalent of a knockout blow for some federal agencies.

The stomach punches and black eyes from the last 12 months of deficit battles already have our country on the ropes. Here’s to hoping that policymakers can regroup and get the fight going back in the right direction.

* All of the numbers and figures in this post are based on projections from the Congressional Budget Office (CBO). However, because the annual cuts actually will be based on up-to-date projections from the Office of Management and Budget (OMB), the numbers included here are estimates.

** For example, as the first table shows, the Congressional Budget Office (CBO) projects that $483 billion of cuts to defense discretionary appropriations (or budget authority) would only reduce outlays by $461 billion through 2021 (the remaining savings would occur, but in later years). To illustrate the timing difference, consider a $100 million aircraft carrier on which construction is scheduled to begin in 2019. Congress appropriates the full $100 million in 2019, but the carrier actually will be constructed over, say, five years ? $40 million will be spent in 2019, and then $15 million will be spent in each of the next four years. While the entire $100 million of budget authority was given inside the ten-year window, the final two years of outlays ($30 million in 2022 and 2023) occur afterward. Therefore, $30 million of the outlay savings from cancelling the procurement would not contribute towards the mandated $1.2 trillion of deficit reduction over ten years (under the latter interpretation of the law). This effect will mean that substantially more than $1.2 trillion (excluding interest savings) of budget authority must be cancelled in order to reduce the deficit by that amount over the ten-year window.

*** The situation for fiscal year 2013 is a bit different from the eight other sequester years that follow. In the latter years, the BCA implicitly conveys cap levels for defense and domestic discretionary spending that Congress must not breach. If they are exceeded, an across-the-board cut eliminates any amount of additional spending. But in 2013, there are no sequester cap levels provided ? just an inevitable hard dollar amount reduction that will be carried out by cutting all line items by the necessary percentage. This means that defense, for example, would face the exact same across-the-board dollar cut if appropriators reduced its 2013 allocation to $100 billion as if they attempted to continue current levels of spending. In addition, our interpretation of the law is that funding for overseas contingency operations will only be subject to the sequester in 2013, while certain other programs are exempt from the sequester only for 2013, such as veterans health care and Pell grants. The unique 2013 case deserves a post of its own and we will follow up shortly.

**** From CBO: “Low-income subsidies and additional subsidies for beneficiaries whose spending exceeds certain levels defined as catastrophic in Medicare’s Part D prescription drug program are exempt from sequestration. (The qualifying-individual program, if funded by future legislation, would also be exempt.) The sequestration percentage cannot exceed 2.0 percent for payments made for individual services covered under Parts A and B and for monthly contractual payments to Medicare Advantage plans and Part D plans. Other mandatory Medicare spending for benefits and administrative costs would be subject to the same percentage reduction that would apply to nonexempt mandatory spending.”

Additional Graphs

Related Posts

- The 2013 Sequester May Not Be What You Think, January 26, 2012

- Three Reasons Why $1.2 Trillion Isn’t Really $1.2 Trillion, January 23, 2012

- Sequester Fact Sheet

- Sequester Presentation

Share

Read Next

Support Research Like This

With your support, BPC can continue to fund important research like this by combining the best ideas from both parties to promote health, security, and opportunity for all Americans.

Give Now