Facts on Long-term Services and Supports

Share

Share

The United States currently lacks a comprehensive and coherent strategy for the financing and provision of long-term care (LTC). Individuals in need of long-term services and supports (LTSS) often face limited coverage and ruinous out-of-pocket costs, and state and federal programs shoulder a growing ? and unsustainable ? financial burden of the long-term care population. Policymakers have long struggled with identifying and advancing viable solutions to our long-term care challenges, and concerns have only heightened in recent years due to an aging baby boomer population, growing strains on federal and state budgets, and increasing disability among working-age Americans.

In January, Congress established the federal Commission on Long-Term Care, charged with developing a plan for the establishment, implementation, and financing of a high-quality long-term care system that ensures the availability of long-term services and supports. The 15-member Commission was created following the repeal of the Community Living Assistance Services and Supports (CLASS) program, a voluntary long-term care insurance program established by the Affordable Care Act (ACA), due to questions about the program’s financial solvency. The Commission held its first meeting in June and has until September 30, 2013 to produce its recommendations. We applaud their efforts to produce a meaningful dialogue around a complex issue. As the Commission continues its work, and policymakers consider options for improving the availability of LTSS, it is important to understand key issues surrounding the debate.

What are Long-term Services and Supports (LTSS)?

Long-term services and supports (LTSS) include a broad range of health and social services that assist individuals who have limitations in their ability to provide self-care. These include assistance with activities of daily living (ADLs), such as bathing, dressing, eating, transferring, and walking and instrumental activities of daily living (IADLs), such as meal preparation, money management, house cleaning, medication management, and transportation.i These services may be provided by nurses, social workers, home health aides, or other formal or informal caregivers to people living at home, in a residential setting such as an assisted living facility, or in an institutional setting such as a nursing home. LTSS are often broken down into two broad categories: institutional and home- and community-based services (HCBS). Medicaid spending for LTSS has gradually shifted towards HCBS in the last decade, largely due to beneficiary preferences and an increasing number of individuals served by Medicaid’s HCBS waiver programs.ii Importantly, LTSS does not include medical or nursing services needed to manage an individual’s underlying health condition.

Who needs LTSS?

LTSS are needed by any person who is unable to perform one or more ADLs, usually due to a physical, cognitive, or chronic health condition that is expected to continue for an extended period of time.iii This population could include a senior citizen who has limited mobility or who has Alzheimer’s disease as well as children born with physical or developmental disabilities, and working-age adults who have inherited or acquired physical or cognitive limitations and need assistance getting ready for work.iv

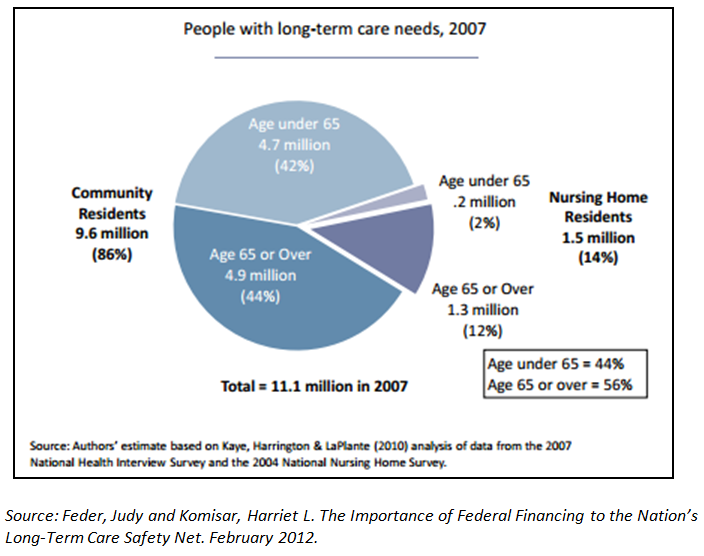

Roughly 11 million adults 18 and older, or 5% of the U.S. population, receive LTSS.v Seventy percent of Americans who reach age 65 will need some form of LTSS in the remainder of their lifetime.vi And by 2050, the number of people needing long-term care is estimated to increase by 70%, to 16.5 million Americans.vii With a significant number of baby boomers expected to retire in the coming years, and as innovations in life extending medicines, technologies and treatments continue to prosper, the demand for LTSS is only expected to grow.

Who provides LTSS?

LTSS can be provided by employees of home health agencies, nursing homes and assisted living facilities but are often provided on an informal basis by friends or family members. In 2009, 62 million family caregivers provided care to an adult with LTC needs at some point during the year, estimated to be valued upwards of $450 billion in unpaid services.viii Informal caregivers often forgo income-generating opportunities, further complicating efforts to save for their own retirement and any future LTSS needs.

Who pays for LTSS?

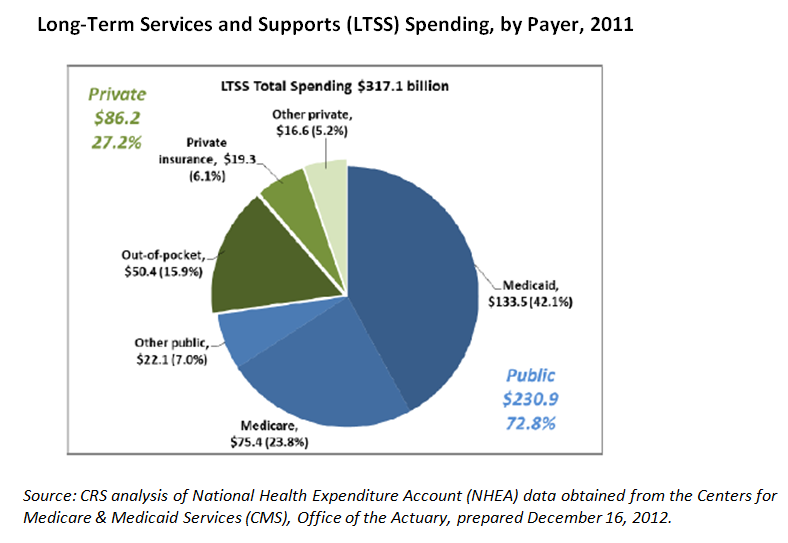

There are three primary means of payment for LTSS: Medicaid; personal, out-of-pocket savings; and private long-term care insurance (LTCI). Medicaid, the federal-state program for low-income beneficiaries, is the nation’s primary payer for LTSS, financing nearly two-thirds (61.4%) of the $210.9 billion spent on LTSS in 2011.ix LTSS accounts for one-third of all Medicaid spending and for 70% of Medicaid spending on “dual eligibles” (beneficiaries eligible for both Medicare and Medicaid).xxi Further complicating matters, LTSS eligibility and coverage vary widely by state Medicaid programs, particularly for HCBS, which, unlike institutional care, is an optional benefit.xii

Individuals are often unpleasantly surprised by the substantial cost of LTSS. In 2012, personal at-home care averaged about $22,000 annually for part-time help; a private room in an assisted living facility averaged $42,000 annually; and nursing home care averaged $81,000 annually for a semi-private room.xiii Many individuals in need of LTSS regularly draw from personal income and assets and rely on family caregivers for a substantial amount of unpaid care and financial support. In 2005, it was estimated that 6% of individuals turning 65 would face $100,000 or more in out-of-pocket LTSS expenses in the remainder of their lifetime.xiv In 2011, individuals and/or families spent $46 billion, or 22% of total LTSS spending, out-of-pocket.xv Many beneficiaries ultimately must exhaust, or “spend down,” their assets in order to qualify for and access Medicaid LTSS assistance, the nation’s primary LTC safety net.

Private long-term care insurance plays a small role in financing LTC services, with only 12 insurers and about 6-7 million policies currently active.xvixvii The private LTCI market has been waning for years, in large part because a majority of individuals are not buying in, citing high premiums, a complex product, and difficulty in qualifying for coverage.xviii Most Americans are not aware that, by and large, Medicare does not cover the cost of LTC. Designed to cover basic health care services ? including hospital stays, post-acute care, physician visits ? and prescription drugs for the elderly and certain individuals with disabilities, Medicare was never intended to finance LTSS. As a result, Medicare only covers skilled nursing facility care or rehabilitation services following a 3-day hospital inpatient stay for up to 100 days, as well as medically necessary, intermittent home health services and physical, speech or occupational therapy services.xix In 2011, Medicare spending on skilled nursing, home health and hospice care reached $64 billion.xx

Considerations for policymakers

In addition to much uncertainty surrounding Medicaid expansion for eligible individuals under the age of 65 and the impact on state budgets, Medicaid programs across the country will soon face the added stress of an aging baby boomer population with low financial savings rates, increasing life expectancy, and increasing prevalence of chronic conditions with functional limitations among the elderly.xxi Growing long-term care needs are putting unsustainable financial pressure on already fiscally strapped states.

Like most policy challenges, there is no simple solution, however some questions to guide the discussion include:

- What are the appropriate roles of public and private entities in the financing and delivery of LTC?

- How can care for dual eligibles be better coordinated and by whom?

- How can public and private resources be better coordinated?

- How can we create a sustainable, affordable, easy-to-navigate long-term care system that provides high quality services while maintaining the dignity, respect and choice of LTSS beneficiaries?

BPC continues to follow the deliberations of the Long-Term Care Commission closely, and we look forward to launching our own initiative on long-term care in the coming months.

i

Alkema, Gretchen E. Current Issues and Potential Solutions for Addressing America’s Long-Term Care Financing Crisis. The SCAN Foundation. March 2013.

ii

O’Shaughnessy, Carol. The Basics: National Spending for Long-Term Services and Supports (LTSS), 2011. National Health Policy Forum, February 2013, http://www.nhpf.org/library/details.cfm/2783.

iii

Colello, Kirsten J., Mulvey, Janemarie, and Talaga, Scott R. Long-Term Services and Supports: Overview and Financing. U.S. Congressional Research Service. April 2013.

iv

Stone, Julie. Long-Term Care (LTC): Financing Overview and Issues for Congress. U.S. Congressional Research Service. February 2010.

v

O’Shaughnessy, Carol. The Basics: National Spending for Long-Term Services and Supports (LTSS), 2011. National Health Policy Forum, February 2013, http://www.nhpf.org/library/details.cfm/2783.

vi

Alkema, Gretchen E. Current Issues and Potential Solutions for Addressing America’s Long-Term Care Financing Crisis. The SCAN Foundation. March 2013.

vii

Tumlinson, Anne. Senior Vice President, Avalere Health. Testimony before the Long Term Care Commission. June 28, 2013.

viii

Alkema, Gretchen E. Current Issues and Potential Solutions for Addressing America’s Long-Term Care Financing Crisis. The SCAN Foundation. March 2013.

ix

O’Shaughnessy, Carol. The Basics: National Spending for Long-Term Services and Supports (LTSS), 2011. National Health Policy Forum, February 2013, http://www.nhpf.org/library/details.cfm/2783.

x

Feder, Judy and Komisar, Harriet L. The Importance of Federal Financing to the Nation’s Long-Term Care Safety Net. Georgetown University, supported by a grant from the SCAN Foundation. February 2012.

http://www.thescanfoundation.org/sites/thescanfoundation.org/files/Georgetown_Importance_Federal_Financing_LTC_2.pdf

xi

David Rousseau et al., Dual Eligibles: Medicaid Enrollment and Spending for Medicare Beneficiaries in 2007, Kaiser Commission on Medicaid and the Uninsured, December 2010, http://www.kff.org/medicaid/upload/7846-02.pdf

xii

Tell, Eileen J. Overview of Current Long-Term Care Financing Options. The SCAN Foundation. March 2013.

xiii

Metlife Mature Market Institute. Market Survey of Long-Term Care Costs: The 2012 MetLife Market Survey of Nursing Home, Assisted Living, Adult Day Services, and Home Care Costs. 2012; https://www.metlife.com/assets/cao/mmi/publications/studies/2012/studies/mmi-2012-market-survey-long-term-care-costs.pdf

xiv

O’Shaughnessy, Carol. The Basics: National Spending for Long-Term Services and Supports (LTSS), 2011. National Health Policy Forum, February 2013, http://www.nhpf.org/library/details.cfm/2783.

xvi

Alkema, Gretchen E. Current Issues and Potential Solutions for Addressing America’s Long-Term Care Financing Crisis. The SCAN Foundation. March 2013.

xvi

Cohen, Mark. Chief Research and Development Officer, LifePlans. Testimony before the Long Term Care Commission. June 28, 2013.

xvii

Stone, Julie. Long-Term Care (LTC): Financing Overview and Issues for Congress. Congressional Research Service. February 2010.

xviii

Tell, Eileen J. Overview of Current Long-Term Care Financing Options. The SCAN Foundation. March 2013.

xix

O’Shaughnessy, Carol. The Basics: National Spending for Long-Term Services and Supports (LTSS), 2011. National Health Policy Forum, February 2013, http://www.nhpf.org/library/details.cfm/2783.

xx

Alkema, Gretchen E. Current Issues and Potential Solutions for Addressing America’s Long-Term Care Financing Crisis. The SCAN Foundation. March 2013.

xxi

Alkema, Gretchen E. Current Issues and Potential Solutions for Addressing America’s Long-Term Care Financing Crisis. The SCAN Foundation. March 2013.

The Common Ground Project provides you with real-time insights into key issues before Congress, what’s holding back passage of legislation, and where there might be common ground.

Share

Read Next

Support Research Like This

With your support, BPC can continue to fund important research like this by combining the best ideas from both parties to promote health, security, and opportunity for all Americans.

Give Now